Week 4: Who’s building these things

I spent this afternoon ( isn’t this your idea of Saturday fun?) trying to line the humanoid companies up for a good ol’ fashioned scorecard comparison, feature by feature, and gave up. Not because the robots are hard to differentiate, but because almost nothing is comparable.

One company’s site leads with a named customer and a count of operating hours on a production line. Another leads with a livestream of a robot sorting packages, a counter ticking past 200,000, with nobody paying for a single one of them to move. A third, Boston Dynamics, makes the most famous walking robot on earth, and you can’t buy it. Every Atlas coming off the line in 2026 is already committed to two addresses: Hyundai, which owns the company, and Google DeepMind, which supplies the AI. No units will be delivered to an outside customer until at least 2027. The most recognized name in the field, and for anyone who isn’t its corporate parent, it isn’t a product. It’s a very well-funded internal pilot.

So you can’t rank these companies the way you would want to, by whose hands are best or whose gait is smoothest or whose demo got more views. The builders and their claims are not answering the same question. Each one is offering a different kind of evidence, and the evidence offered does not create a like-for-like playing field. Capability footage is one currency. A funding round is another. A unit-shipment count is a third. Operating hours at a named customer is a fourth. Before you can read this landscape at all, you have to know the exchange rate between the currencies.

It helps to see what each currency is worth. Humanoid startups raised about $3.2 billion in 2025, more than the previous six years combined, by Dealroom’s count. Figure alone carries a valuation near $39 billion, more than ten times what the entire sector raised that year. The best demo videos clear millions of views in a weekend. Set that against a different currency, the one that is most meaningful: Counterpoint estimates about 16,000 humanoid robots were installed worldwide in all of 2025, and more than 80 percent of those were in China, mostly not at the companies getting the headlines.

Billions of dollars and millions of views on one side. Sixteen thousand machines on the floor on the other.

What follows is my attempt at a first-pass vendor map. It is built from product pages, press releases, and earnings calls, not from gemba time, so I’ll get some of it wrong and update when I do. Last week I sorted these machines by what they are: logistics movers, station manipulators, mobile manipulators, teleoperated bodies. This week I’m sorting the companies by evidence. Let’s consider three questions.

Three questions

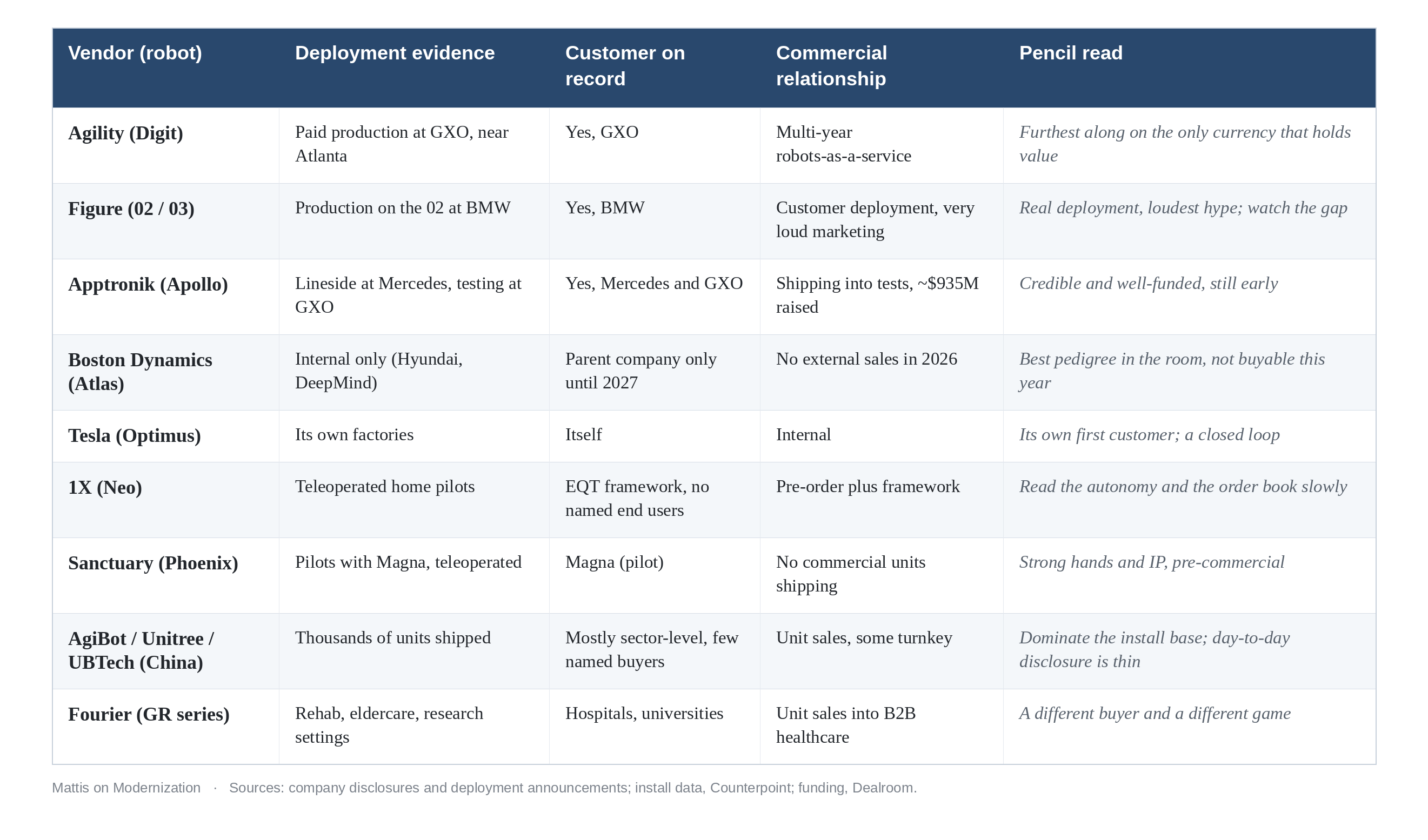

First: is there deployment evidence? The bar is specific: is there a robot doing repetitive, unglamorous work at a named site, under production conditions, for long enough that someone can quote you operating hours, with money changing hands for the work. Agility’s Digit shines in answer to this question: it has been moving totes onto conveyors at a GXO warehouse near Atlanta under a paid, multi-year robots-as-a-service deal the two companies call the first formal commercial humanoid deployment. Figure has comparable evidence, on its older robot: Figure 02 ran about eleven months on the BMW line at Spartanburg, roughly 1,250 operating hours across 10-hour weekday shifts, contributing to more than 30,000 vehicles. What doesn’t count, however polished, is a livestream counter or a six-minute home video. The test is dull on purpose. The question that needs to be answered is “would a customer pay to have this exact work done, and can you show that they are?”

Second: will a customer go on record? A buyer that puts its name and its logo on your robot is wagering reputation, which is why disclosure is the evidence that’s hardest to fake. GXO names Agility on its own earnings calls. Its year-end note said it would “steadily increase” robotics deployment in 2026, which is the phrasing of a buyer hedging, not a buyer evangelizing. BMW is named at Spartanburg. Mercedes both invested in Apptronik and is testing its Apollo. And the most useful tell in the whole market: GXO is running both Digit and Apollo. When the most credible customer in the category is hedging across two vendors, that says how early it is more honestly than any roadmap slide. The weak version of this signal is “a leading global logistics provider,” unnamed. When the customer won’t be named, assume pilot.

Third: what is the commercial relationship? Pilot, framework, and paid production are three different things that get reported in the same sentence. Agility’s GXO arrangement is paid production, which is close to the top of the field. Most of the rest is softer than the headline. When 1X announced a deal to put up to 10,000 of its Neo robots in front of an investor’s 300-plus portfolio companies by 2030, much of the coverage treated it as an order book. It’s a framework to negotiate individual deals, which is a different object. A framework is a maybe with a press release.

The field

A few of these deserve more than a row, so I’ll expand here.

Boston Dynamics and Tesla are the same shape, for opposite reasons. Boston Dynamics has the deepest engineering history in the room and has committed every unit to its own parent. Tesla is converting part of Fremont to build Optimus and its only disclosed customer is itself. Both are running closed loops. Being your own first customer is a legitimate way to start: you control the building, the data, and the blame. It is also not the same evidence as an outside buyer choosing to pay, and Musk’s prediction of thousands of Optimus units in Tesla’s own plants by the end of 2025 is a fair reminder of how these calendars move.

1X and Sanctuary are where the word “autonomous” needs reading glasses. Neo ships to homes now, for $20,000 or $499 a month, but the early units run with a human in the loop, a remote operator stepping in when the robot can’t cope. You’re buying a robot plus a person, which is a different cost and privacy model than the ad implies. Sanctuary’s Phoenix runs on the same engine: genuinely impressive hands, pilots with the parts maker Magna, teleoperation underneath, and no commercial units shipping yet. Neither is a scandal. Teleoperation is a reasonable bridge to autonomy. It is just not autonomy, and the price of the robot is not the price of the service.

Then there’s the cohort most North American coverage barely registers. The single largest shipper of humanoids in 2025 was not Figure or Tesla. By Counterpoint’s count it was AgiBot, a Shanghai company most US operators have never heard of, with roughly a third of global installations on the strength of mass-produced units sold into hospitality, manufacturing, and logistics. Unitree shipped more than 5,500, with a sub-$20,000 machine and a target of 20,000 this year. UBTech put its Walker S2 into mass production and reported orders worth roughly $112 million, much of it for automotive plants. XPeng, the EV maker, is sitting on a large cash pile and pointing it at humanoid production. Fourier is a different animal again: it came out of rehabilitation robotics and sells into hospitals, eldercare, and research, not warehouses. The volume is real and it dwarfs US output. What I can’t see from here is the part that matters most: what those thousands of units do on an ordinary day, and how often they break. The Western vendors over-disclose capability footage. This cohort over-discloses volume. Neither one tells you the uptime.

What I don’t know

I can’t independently verify any of these deployment claims. I’m reading announcements and earnings calls, not standing on the floor watching the thing run for a week.

Nobody publishes the number that would settle most of the argument: uptime, or mean time between failures, under production conditions. A forklift vendor will quote you that without being asked. Until a humanoid vendor does, every “deployed” carries a quiet asterisk.

The teleoperation percentage is mostly undisclosed too, and it’s decisive, because a robot that’s ten percent piloted and one that’s ninety percent piloted are different products with different economics wearing the same shell.

Even the market’s headline number comes in incompatible currencies. One firm counts 16,000 installations, another counts 18,000 shipments, a third counts $440 million in revenue, and they are measuring three different things. And funding, the loudest number of all, tells you about runway and investor conviction. It tells you nothing about whether the robot works on a Tuesday in a building that smells like a warehouse.

Missing pieces

So before I told a customer to take any of these companies seriously, I’d want five things, and it’s the same evidence for each company:

A named customer, on the record, who’ll take my call and tell me what broke.

Operating hours under production conditions, not demo conditions, with the gap between the two stated honestly.

The teleoperation percentage, in writing.

Total cost, not unit price: integration, support, the service model, and who owns the failure when it happens.

A boring answer. The vendor whose materials are thick with dull operational detail is almost always further along than the one with the better sizzle reel, because the dull detail only exists once someone has successfully operationalized the robot.

If you’re being pitched one of these robots in the next year, take this list into the meeting and let it do the work. Run the three questions and the five asks against the deck in front of you, and watch which currency the vendor reaches for when you press. The ones paying in operating hours and named customers will keep talking. The ones paying in funding rounds and view counts will change the subject.

Somewhere a facilities lead or an automation manager is going to be handed one of these robots and told to keep it running long after the announcement scrolls off everyone’s feed. That person doesn’t care what the company was valued at. They care whether the robot works and is supported on Tuesday. My vendor map isn’t a ranking, it’s a list of currency exchange rates, and right now the rarest, most valuable currency in the field is also the simplest: a named customer who’ll tell you the truth about what broke.

Views are personal and do not represent any employer, past or present.